A decade after Britain voted to leave the European Union, the economic verdict is increasingly difficult to contest. Writing in the Guardian, senior economics correspondent Richard Partington finds that while the immediate recession predicted by then-Chancellor George Osborne never materialised, experts broadly agree that Brexit has resulted in sustained and significant costs for households, businesses and the wider economy.

Charlie Bean, a former Bank of England deputy governor who reviewed the Treasury's original forecasts, told Partington that Osborne had overstated the short-term danger, handing Leave campaigners an easy point of attack when no immediate collapse followed the vote. But Bean said the longer-term assessment had proven accurate: "We're poorer than we otherwise would have been."

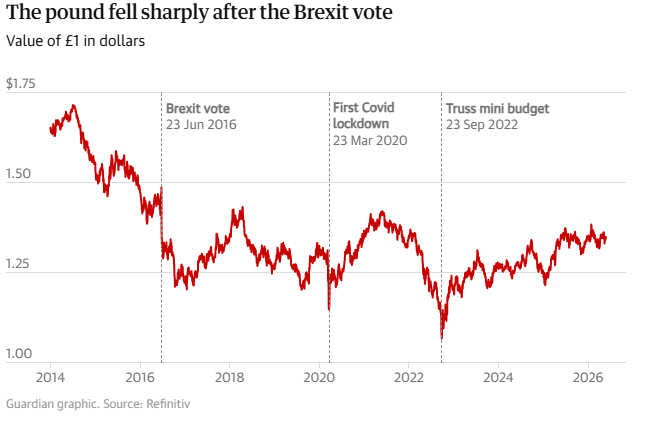

The pound has never recovered to its pre-referendum level. On the night of the vote, sterling fell 10% in a single session, its largest ever one-day drop. Today it stands at $1.34 against the dollar and €1.15 against the euro, down from roughly $1.50 and €1.31 at the time of the vote. The collapse in sterling drove up import costs and triggered an inflation shock that damaged public finances and squeezed household budgets for years.

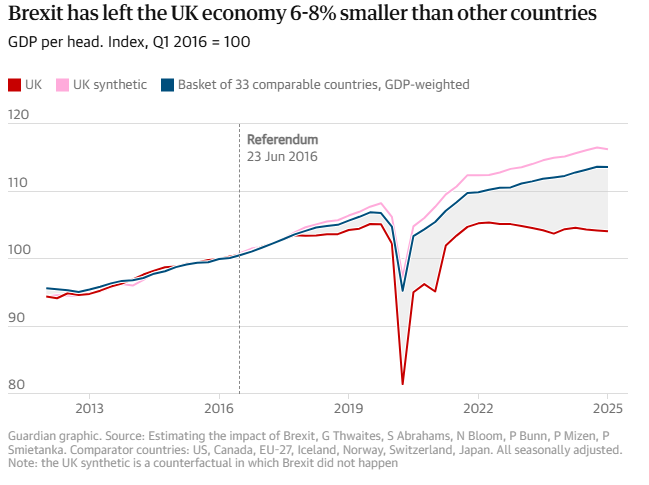

According to the Office for Budget Responsibility, Britain's independent fiscal watchdog, the UK is on course to suffer a 4% hit to national income over a 15-year period. Research by Nick Bloom, a prominent British economist at Stanford University, goes further, estimating that GDP per head is between 6% and 8% lower than it would have been under a remain scenario, based on a comparison with 33 other advanced economies that tracked closely alongside Britain until 2016 before diverging sharply. Bloom told Partington he saw no explanation other than Brexit for the gap.

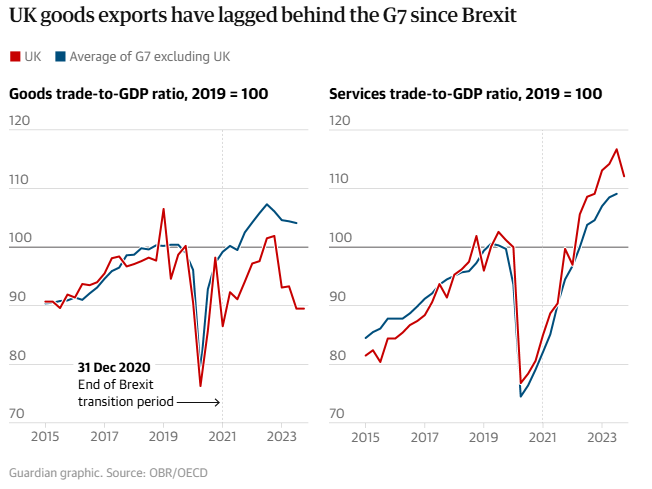

Trade has also suffered. The EU remains Britain's largest trading partner, acc ounting for 41% of UK exports and 49% of imports in 2025. Since the end of the transition period in December 2020, growth in goods exports has slowed markedly relative to other G7 economies, with exporters facing more red tape and border delays than before. Service exports have held up better, which the OBR attributes to Boris Johnson's trade and cooperation agreement creating more friction for goods than for services.

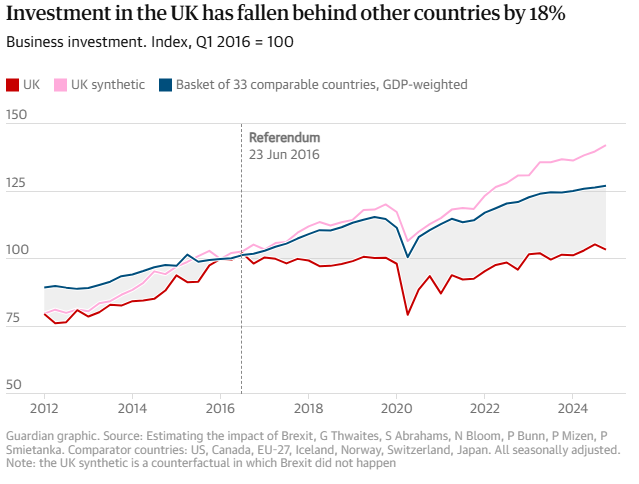

John Springford of the Centre for European Reform told Partington the damage had come gradually rather than in a single shock, describing Brexit as "more a story of stagnation, and a slow puncture, than of recession and rising unemployment." Business investment is estimated to be close to 18% below where it would have been under remain, and productivity up to 4% lower. Bloom estimates employment is between 3% and 4% lower than it would have been, and Britain recorded the worst recovery in workforce participation among G7 countries after the pandemic, with the number of 16-to-24-year-olds not in education, employment or training climbing above one million, the highest level since 2013.

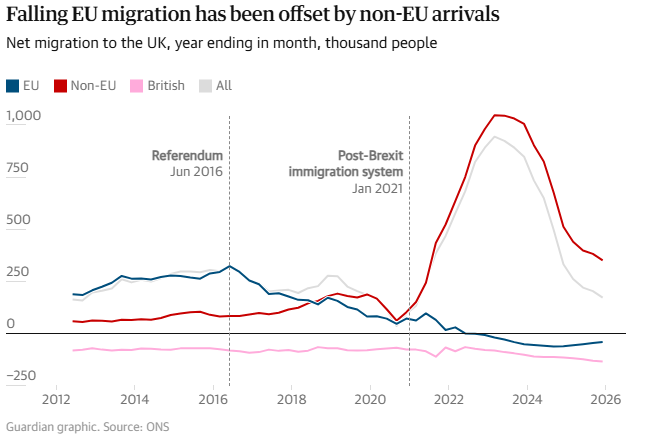

The promised reduction in immigration also failed to materialise in the near term. Net migration rose sharply after Brexit, reaching a record of close to one million in the year to June 2023. Almost 90% of arrivals came from outside the EU, while net migration from EU member states fell, leaving employers in construction, hospitality and manufacturing struggling with labour shortages. Net migration has since dropped to 171,000 last year following tightening of controls under both Conservative and Labour governments.

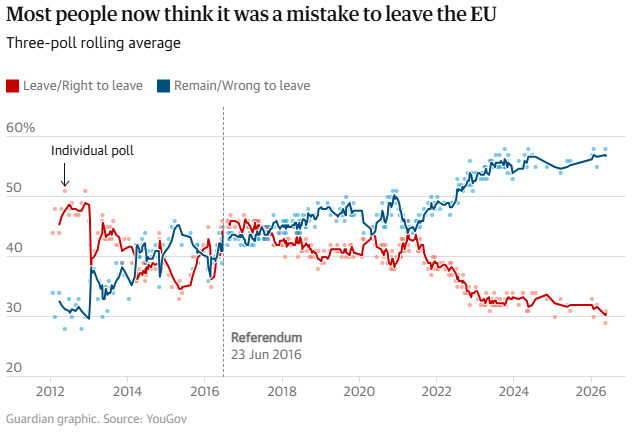

Public opinion has shifted considerably since the 52%-48% Leave vote. A YouGov poll last month found that 70% of Britons support a closer relationship with the EU short of rejoining, and that a majority, 56%, would now back full membership.

Source: The Guardian